Are You Planning to Fail?

Happy Sunday!

Are You Planning to Fail?

The kids are back in school, fall is just around the corner, and the deer are still out in the fields because they know hunting season hasn’t started yet. Not having two kids running around the house while we are working feels a bit strange for my wife and me, but with productivity at an all-time high, we enjoyed a Friday lunch date at a local burger joint.

Anyway, for this weekly newsletter, we’re going to talk planning. You already know that plans fall apart as soon as they are completed, but it’s the planning process that gives you the highest chance of achieving your objectives.

Financial planning is something that never seems to make it onto our to-do list; it stays on the should-do list instead. We’re going to talk through the process so you can spend more of your time on things you value and less time spinning your wheels.

Before we dive into this week’s topic, here are three things I read this week that I thought you’d like

WSJ – Synapse Bankruptcy

I’m sending this to you because it’s a great example of the dangers associated with FinTech and banking.

The Weekly Sitrep - Taxes and How to Reduce Them

I’m sending this to you because it takes a deeper dive into tax planning. The Weekly Sitrep regularly posts competitive SkillBridge internships and high-paying job postings.

Housel – A Number From Today and A Story About Tomorrow

I’m sending this to you because it discusses the fallacy of accurately predicting the future and how compelling stories are used to convince investors otherwise.

Let’s dive in!

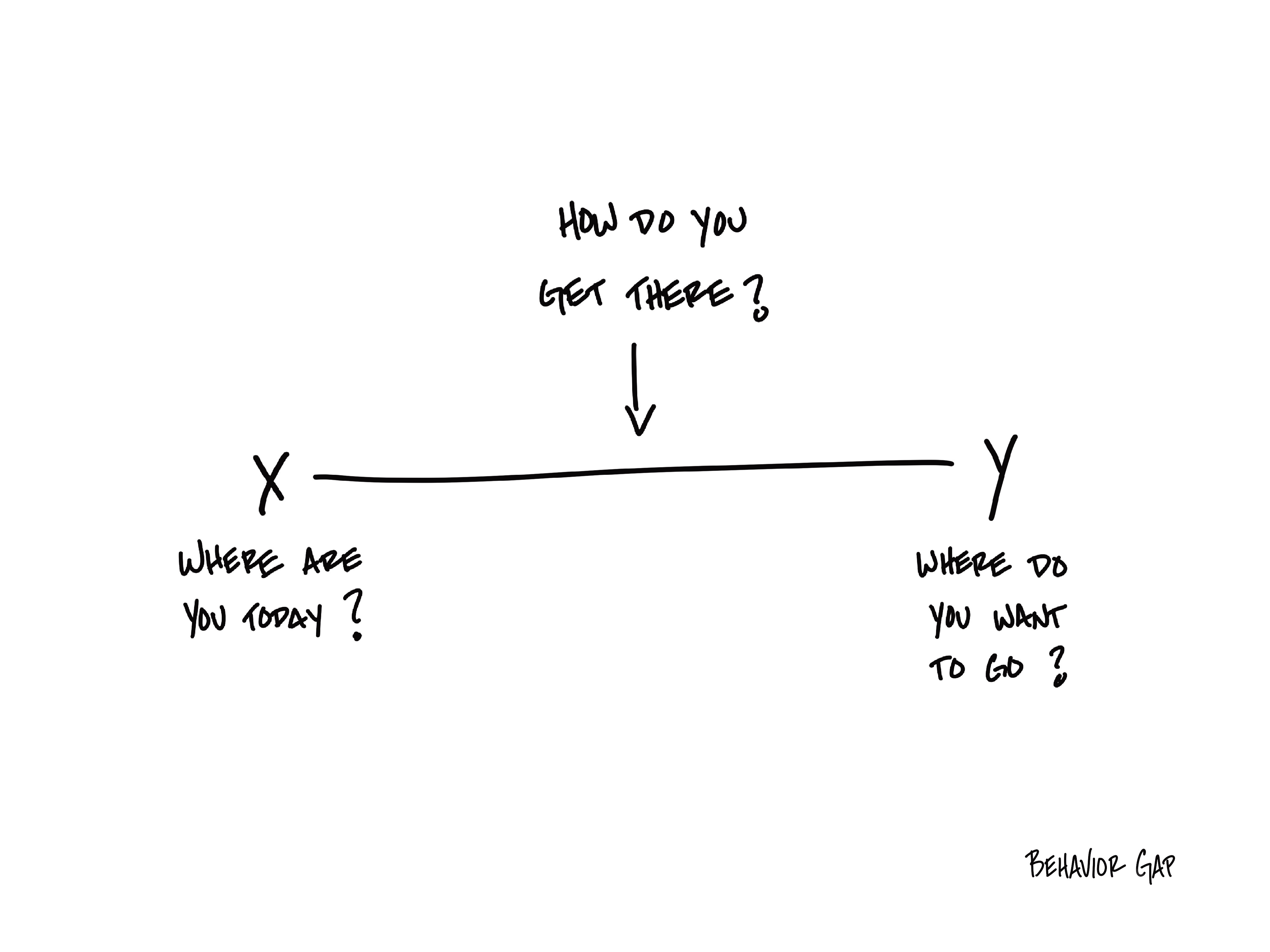

This month’s theme is PLANNING. When we do financial planning, we are trying to answer three broad questions:

Where are you today?

Where do you want to go?

How do you get there?

This week I’m going to give you the tools to answer that first question. Although math matters, complete accuracy does not move the needle when it comes to these questions. Don’t feel like you have to be accurate to the penny, you can round to the nearest thousand if you’d like.

Where are you today?

Your MBA probably taught you about balance sheets and income statements.

Companies have them and so do you. These matter because they are the inputs to your financial plan, and they are the most accurate information you have about where you stand today.

Balance sheet

One of your biggest assets is probably your home equity, and it’s also probably the one you have the most clarity on. Next comes all your investment assets, and we break these into categories: taxable or tax-advantaged. Tax-advantaged includes both tax-deferred accounts like the traditional versions of your TSP, 401k, and IRA and tax-free or Roth versions of these accounts. Then we break up each account into its approximate holdings: stocks, bonds, and cash.

Here’s the format I use to visualize these account balances. This helps me see if accounts make sense at the 30,000 foot level. Are they spread all over the place? Are there strange allocations? Can we simplify? This is also the easiest way to determine if we have missed something important.

Next, list out all your personal debts. This list is usually a bit less complicated, and there’s no shame here. Debt is a tool, sometimes we use it wisely and sometimes we don’t. We all make stupid decisions with out money at some point, but let’s not omit things because you’re embarrassed. Next to all your debts, write out the monthly payment and how many more years until the debt is paid off.

Finally, add your assets and liabilities together to determine your net worth.

Income Statement

Let’s make this one super simple:

Total Compensation – Savings – Taxes = Living Expenses

So if you’re making $300k as a household, saving $60k per year, and paying $120k in taxes, then your living expenses are about $120k. No need to get super complicated at this point. We just want to identify the big blue arrows.

Your current living expenses are likely your benchmark for how much you want to live off later in life. You’ll adjust up or down from this number, but unlike all the other numbers, you actually know what this one looks like and feels like to live on.

Bringing it Back

At the end of the day, financial planning isn’t just about crunching numbers, it's about designing the life you want to live. Knowing where you are today is the first step in this journey. By taking an honest look at your balance sheet and income statement, you can start making informed decisions that align with your long-term goals.

Next week, we’ll dive into “Where do you want to go?” helping you define the milestones that matter most to you. In the meantime, take some time this week to reflect on your financial position and make sure you’re clear on the big picture. After all, no one else is going to take control of your financial future but you.

Hope you have a great week.

-Henry