Education - 529 vs Taxable Account

Happy Sunday!

Education - 529 vs Taxable Account

After years of saying fishing was boring, I finally went out and learned to fly fish. Not sure if it was the beautiful weather or just spending the day with my brother by the river, but fly fishing was pretty fun!

It’s not replacing shooting as my main hobby, but there was something very relaxing about fly fishing.

Last week’s newsletter highlighted the financial costs of private education. This week we’re going to break down some of the most popular ways to save for that education and make it a bit less financially painful.

Before we dive into this week’s topic, here are some things I thought you’d like:

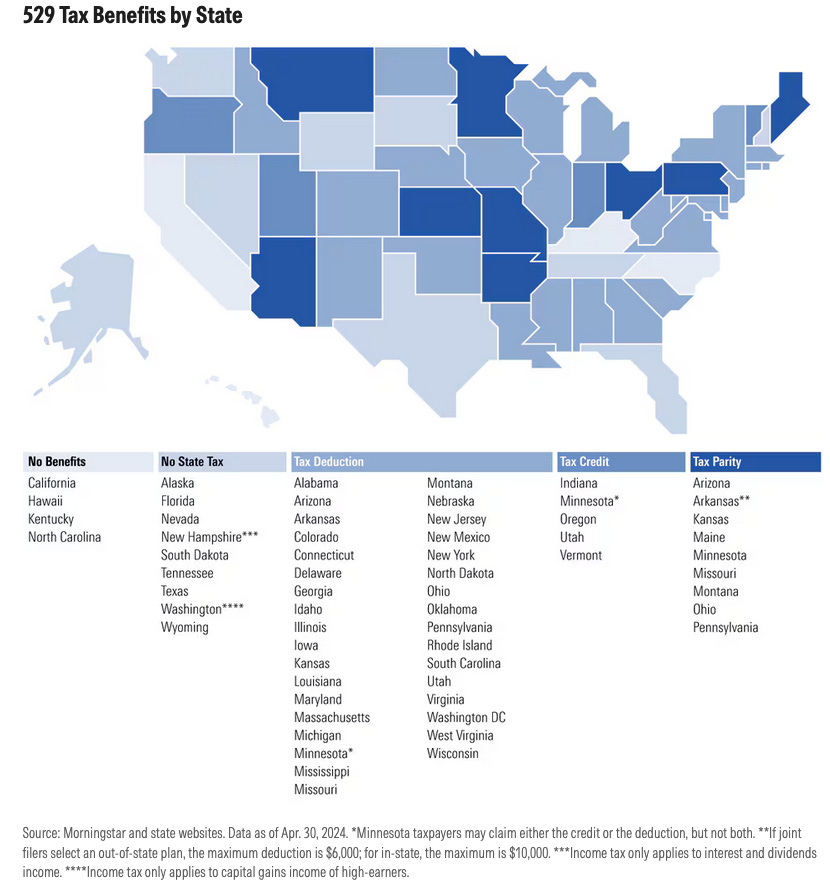

Morningstar - Understand Your 529 State Tax Benefits

Want a more clinical description about 529 plans state tax credits that isn’t tailored to MBA Vet Families? Morningstar has your back.

Kitces – Using a Family Dynasty 529 Plan for Multigenerational College Planning

I write for you. This article is written for me. Grab 2 more cups of coffee before clicking this link.

AP – National Guard Helicopter Crew Landed on Montana Ranch and Trespassed to Take Antlers

Just the National Guard doing redneck stuff.

Let’s dive in!

This month’s topic is EDUCATION.

You’ll get an education in education and become better educated. Here’s what we’re covering:

How Much it Costs

529 Plans vs. Taxable Accounts

529 Plan Specifics

Advanced Education Planning

When it comes to education funding, families typically rely on some combination of savings and loans. Before we talk about where to save, let’s briefly talk about when borrowing makes sense.

Student Loans.

Yup, borrowing the money.

Debt gets a bad rap, but student loans aren’t the end of the world.

When used as a tool, debt can be phenomenal. The problem is that helping pay for your children’s education can be a hugely emotional decision, and when it comes to large financial decisions, emotion is one player I don’t want at the table.

We’re not going to dive into the sea of student loan options, but there are a few big takeaways I want you to remember when it comes to student debt.

Borrowing for pre-college expenses is probably going to overextend your family financially.

In a low-interest rate environment, student loans could be the golden ticket to a great education. In a high interest rate environment, less so. Especially since interest rates are a bit cyclical and you may be on the opposite end when it’s time to pay them back.

And maybe most important: Your child can borrow for their education, you can’t borrow for your retirement.

Remember, debt is a tool. Use it intelligently, not emotionally.

If you decide that savings will do the heavy lifting, the two main vehicles to consider are 529 plans and taxable brokerage accounts.

529 College Savings Plan.

Next week we’re going to do a deep dive on 529 College Savings Plans, but here are the basics you should know.

A 529 College Savings Plan is a federally recognized tax-free account that exists at the state level. Each state administers their own plan, and some states offer more than one.

You could also access these plans through a financial advisor, but that’s probably going to increase your costs and they take about 5 minutes to set up on your own.

You can think of a 529 plan like a Roth IRA but for education rather than retirement.

Contributions are made with after-tax dollars.

Growth is tax-free.

Withdrawals are tax-free when used for qualified education expenses.

So, sounds a lot like a Roth IRA to me……

Except that you can contribute to them even if you’re making $500k per year!

And what counts as a qualified education expense?

Tuition and fees

Books and supplies

Computers and internet

Up to $10k/year in K-12 tuition per child (state dependent!)

Room and board (if enrolled at least half-time)

Some student loan repayment

Remember I said it was a state-level plan? Well, some states provide tax breaks in the form of credits or deductions to incentivize college saving. The tax breaks are just at the state level, but depending on your state they can be meaningful.

Even without a state tax incentive, the federal tax advantages alone can make 529 plans worthwhile.

Just remember, these are education savings plans, so non-qualified withdrawals are penalized with lovely things like income tax and a 10% penalty.

Ouch!

So where else could you save for college that offers a bit more flexibility?

Enter the taxable investment account.

Taxable Brokerage Accounts.

Also known as brokerage accounts, these taxable accounts are one of the core financial accounts you’ll own as a responsible adult.

They don’t offer the tax-free growth that 529 plans offer, but there’s one area where they smoke the competition: flexibility.

In a taxable account:

No annual contribution limit

Interest and dividends are taxed in the year earned

Gains are taxed at sale, hopefully at the long-term capital gains rate

This flexibility matters a lot though.

If your child decides not to go to college, or gets a full scholarship, or simply doesn’t need as much as expected, you might be left with an overfunded 529 plan that could be hit with penalties for withdrawing.

But, extra college savings in your taxable account could go towards a car, helping with a downpayment, or just taking the family on ski trips.

When I build a financial plan that involves education saving (spoiler: nearly all the plans I build do), I initially plan to fund 50% of the college goal with a 529 plan and the rest with taxable assets.

This gets adjusted depending on factors like: number of children, income trajectory, state tax benefits, and other planning goals involving gifting.

529 plans offer tax efficiency.

Taxable accounts give you flexibility.

A mix gives you optionality.

Bringing it back.

Here’s what to remember from this week:

· Your kids can borrow for college. You can’t borrow for retirement. Prioritize your financial stability first.

· 529s are tax efficient but a bit rigid. They’re a great tool for tax-free growth, especially if your state offers incentives.

· Taxable accounts are flexible. No tax penalties for changing course later on.

Saving for college now is a gift to both your future self and your kids. But how you save is just as important as how much you save, and we’re going to get into some more advanced education planning material over the next couple weeks.

This whole month’s topic was inspired by one of my amazing client families who wanted to learn a bit more about education planning.

If there’s something you’ve been wondering about, send me a message. I love tailoring content to what actually matters to you!

Hope you have a great week.

-Henry

The content shared here does not constitute financial, legal, or any other professional advice. Readers should consult with their respective professionals for specific advice tailored to their situation.