$ Architecture – Structure

Happy Sunday!

$ Architecture – Structure

The Preston family went on a trip, the girls each caught tons of tuna (our 5 year old’s first fish), and we caught this bad boy.

Also, despite her seasickness, Alyssa kept her breakfast down.

So wins all around.

Our Captain was amazing at getting the girls on fish, and we couldn’t have done it without him.

For reference, below is one of the fish I caught last year.

Blown up to about 1,000,000x so you can actually see it dangling from the fly in it’s mouth. I’d like to thank my friend who sent this as a reminder of my fishing skills.

Let’s dive in!

This month is about $ Architecture, what your balance sheet is and what it could be. We’re covering:

Structure

Purpose

Prioritization

Why this topic?

Because I consistently meet really high-earning and brilliant Veterans with MBAs screwing it up.

And I don’t want you to be in that group anymore.

Structure.

Most families don’t intentionally design their financial systems.

You accumulate them over time.

And over enough years, life gets complicated.

You change jobs. You move. You get married. You open a joint account. You leave behind old 401ks. You accumulate equity compensation portals. You open a brokerage account to do some day trading. You inherit an IRA. Oh and your spouse has accounts at three different custodians.

Then one day you sit down to “look at the finances” and realize your household balance sheet is a mile long and 15 logins deep.

Sounds like a subscription for 500mg Advil is in your future.

Nothing is coordinated. Nothing pulls in the same direction. Half the accounts were opened for reasons you barely remember.

And it creates friction.

Not catastrophic friction, just enough friction that things slowly become inefficient.

Cash sits in the wrong place. Investments overlap. Nobody knows what account is for what. You and your spouse need a 90-minute sync meeting just to figure out what you own.

That’s exhausting, and more importantly, it consumes your limited mental bandwidth.

Just because you’re complex doesn’t mean your finances have to be confusing.

You can intentionally structure things so you have the bandwidth to deal with complex problems when they inevitably arise.

That’s the point of good financial architecture.

Elegant simplicity creates bandwidth and mutual understanding.

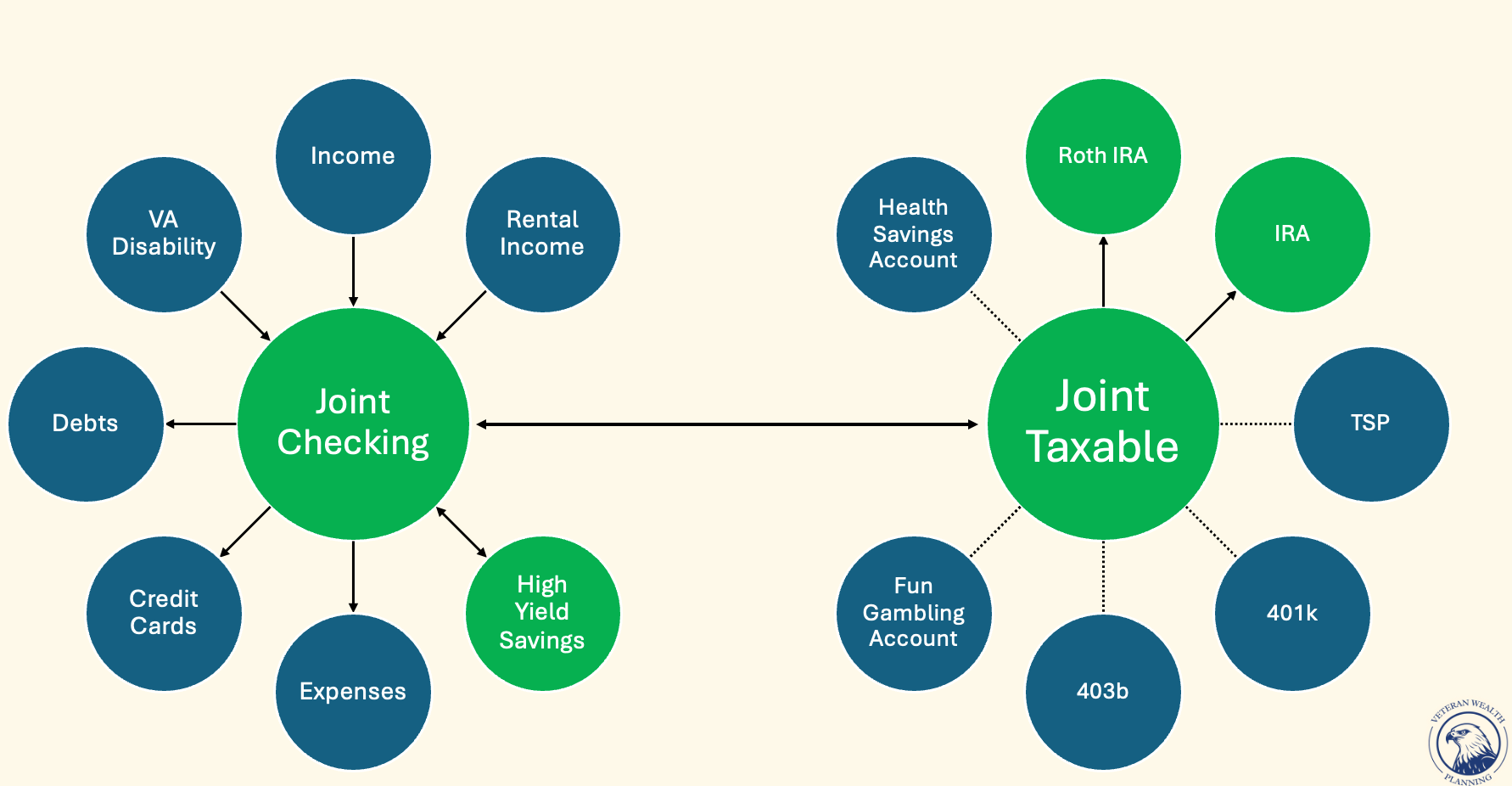

Hub and Spoke.

The easiest way I’ve found to explain this is through a hub-and-spoke framework I use in an MBA Veterans Club presentation.

On the left side of the system, you have your CASH MANAGEMENT infrastructure.

At its center sits your joint checking account.

That’s your CASH HUB.

Income flows in. Bills flow out. Credit cards get paid. Automatic transfers happen. Peace in the Middle East.

Then connected to that hub are the spokes:

High-yield savings

Credit cards

Business operating accounts

Property accounts

Etc

But each account has a role. If it’s redundant, then it’s not there. Think, big-tech layoffs (blamed on AI and McKinsey) but for your balance sheet.

Then on the right side, you have your INVESTMENT infrastructure.

The hub there is a joint brokerage account or revocable trust account. The latter likely replaces the former after your estate planning is complete.

Again, this becomes the center of your investments.

Then the spokes branch off:

Roth IRAs

Traditional IRAs

401ks

403bs

HSAs

529 plans

Equity compensation plans

Irrevocable Trust accounts

Custodial accounts

ESPP

You get the picture

The point isn’t to minimize the number of accounts at all costs.

The point is intentional organization that reduces unneeded complexity.

Because every additional account introduces:

Another login

Another statement

Another place for cash to accumulate accidentally

Another place for investments to drift

Another point of confusion for your spouse

And eventually that complexity compounds.

Now, this doesn’t mean every family needs the exact same structure.

A dual-military family with pensions, VA disability, children, and rental properties will likely have a different structure than a young and single startup founder with concentrated equity comp.

That’s normal.

But coordinated systems beat random account buckets.

Structure Enables Automation.

One of the biggest advantages of good architecture is automation.

Because once accounts are coordinated correctly, money can begin moving automatically.

Paycheck hits the CASH HUB.

Credit cards come out of the CASH HUB.

Automatic transfers move excess cash from your CASH HUB to your INVESTMENT HUB at month end.

Goldilocks levels of cash without having to helicopter parent your balance sheet.

Now instead of constantly moving money, you’re supervising the system.

MBAs often think that complexity is sophistication.

It isn’t.

A clean system that consistently works beats your idea of a hyper-optimized mess.

Equity Compensation.

This problem only gets more pronounced when you throw multiple layers of equity comp into the equation.

12 stock option grants at your current employer

Old ESPP accounts

Multiple custodians

Random legacy retirement accounts

Exercised ISOs here

Partially vested RSUs there

And if the rest of your balance sheet isn’t organized, this just throws gasoline on the fire.

So we’re looking for a consolidated system rather than a random collection of accounts.

One more important point: Good structure is not just about efficiency.

It’s also about resilience.

If something happened to you tomorrow, could your spouse realistically step in and understand the system on day one?

Or would they be left sorting through:

19 accounts

4 custodians

3 password managers

2 old employers

And a pile of unopened mail on the floorboard of your truck

Yeah, let’s avoid that mess.

Bringing It Back.

The purpose of good financial architecture is not over-simplification but elegant simplicity.

It reduces friction.

Increases visibility.

Enables automation.

And ultimately creates enough mental bandwidth that you can focus on the parts of life and planning that actually deserve your attention.

Next week we’ll discuss PURPOSE.

Plain English around what all these different accounts are actually supposed to do inside your financial system.

Hope you have a great week.

-Henry

The content shared here does not constitute financial, legal, or any other professional advice. Readers should consult with their respective professionals for specific advice tailored to their situation.